Budgeting, 50/30/20 Rule And Investment Strategies

Today, we have Suzanne Wanjiko, founder of Legacy Hub KE, a coaching company specializing in personal finance, business coaching, and life coaching, shares her expertise on budgeting with 50/30/20 Rule and investment strategies. As an investment portfolio management professional and certified life coach, Suzanne is passionate about helping individuals achieve financial freedom. In this session, she delves into the importance of budgeting, understanding your risk appetite, and identifying the right investment options.

Demystify Budgeting

Many people misunderstand budgeting, often equating it to simply listing bills. However, Suzanne emphasizes that budgeting goes beyond this. While listing expenses like rent, electricity, utilities, and transport is a start, it doesn’t guarantee financial stability. Many individuals who follow this approach still struggle with saving, investing, or breaking free from debt.

So, what is budgeting? Suzanne defines it as the process of telling your money where to go instead of wondering where it went. It is the cornerstone of financial freedom. While it may seem like a small step, budgeting holds immense power in helping individuals understand and control their spending habits.

The Spending Problem

One of the key insights Suzanne shares is that financial struggles are often not due to a lack of income but rather a spending problem. She highlights a common phenomenon: as income increases, so do expenses. This is known as lifestyle creep. For instance, someone who once managed on a modest income may find themselves struggling even after earning significantly more. This cycle perpetuates the paycheck-to-paycheck lifestyle, regardless of income level.

Budgeting helps address this by focusing on spending habits. It ensures that as income grows, individuals allocate their resources wisely, avoiding unnecessary expenses and prioritizing financial goals.

The Four Essential Components of a Budget

Suzanne outlines four critical components that every effective budget must include:

- Mandatory Bills and Expenses

These are non-negotiable expenses such as rent, electricity, utilities, transport, gym memberships, and school fees. They must be accounted for in any budget, as they are essential for daily living. - Debt Repayments

If you have debt—whether it’s student loans, mobile loans, mortgages, or personal loans—it’s crucial to allocate a specific amount or percentage of your income toward repayment. Suzanne advises against waiting for a lump sum to pay off debt. Instead, consistent, planned repayments should be part of your budget. - Savings

Savings are essential for capital preservation. They are ideal for short-term goals, such as projects spanning three to six months. However, Suzanne cautions against relying solely on savings for long-term financial growth due to the impact of inflation. Savings can be held in banks, insurance policies, or other secure platforms. - Investments

Unlike savings, investments are about putting your money to work. Investing not only preserves capital but also generates returns, helping you build wealth over time. Suzanne stresses that while saving is important, true financial freedom comes from investing.

Practical Tools for Budgeting

To help individuals implement these principles, Suzanne use multiple tools with clear framework for allocating funds across mandatory expenses, debt repayments, savings, and investments.

Suzanne’s session underscores the importance of budgeting as a foundational step toward financial freedom. By understanding where your money goes and making intentional decisions about spending, saving, and investing, you can break free from the paycheck-to-paycheck cycle and build a secure financial future.

The Importance of Investing and Managing Wants

Suzanne Wanjiko continues her insightful discussion on personal finance by emphasizing the critical role of investing in achieving financial freedom. She explains that while saving preserves capital, investing multiplies and grows your money. This distinction is vital because inflation—the rate at which prices of goods and services increase annually—erodes the value of uninvested money.

For instance, if inflation hit 5%, the cost of living rises by that rate each year. If your money isn’t growing at least at the same pace, your purchasing power diminishes. This means you’ll struggle to maintain your current lifestyle, let alone improve it. Suzanne highlights how rising fuel prices, for example, trigger a chain reaction, increasing the cost of nearly everything. Unfortunately, most employers don’t adjust salaries to match inflation, making it essential to invest wisely.

Investing ensures your money not only keeps up with inflation but also surpasses it. This allows you to sustain your lifestyle and, over time, improve it. Suzanne stresses that long-term investing is particularly powerful, as it generates passive income—money earned without active effort. Imagine receiving dividend or interest payments while you sleep! This passive income stream complements your primary earnings, providing financial security and freedom.

The Four Pillars of a Budget

Suzanne reiterates the four essential components of a budget:

- Mandatory Bills and Expenses

These are non-negotiable needs, such as rent, utilities, and transport. - Debt Repayments

Allocate a specific amount or percentage of your income to pay off debts, whether they’re student loans, mortgages, or personal loans. - Savings and Investments

Savings are for short-term goals, while investments are for long-term wealth building. - Entertainment, Wants, Leisure, and Giving

This category covers discretionary spending, such as travel, dining out, and social events.

Distinguishing Between Needs and Wants

Suzanne shares a practical rule of thumb for differentiating needs from wants: If your income were halved, which expenses would you cut? The items you’d sacrifice are wants, while those you’d retain are needs. For example, eating out or getting massages are wants, whereas rent and utilities are needs.

She advises allocating a specific portion of your budget to wants, leisure, and giving. This includes social events like birthdays, anniversaries, and baby showers, as well as miscellaneous spending for unforeseen expenses.

The Role of Miscellaneous Spending

One of the most common budgeting challenges is unexpected expenses derailing financial plans. Suzanne emphasizes the importance of including a miscellaneous category in your budget. This allocation creates flexibility, ensuring that unforeseen costs—like car repairs or medical emergencies—don’t disrupt your savings or debt repayment plans.

The amount set aside for miscellaneous spending depends on your lifestyle and income. Whether it’s 3,000, 10,000, or 20,000, having this buffer is crucial. It prevents you from compromising on essential financial goals when unexpected expenses arise.

Suzanne’s approach to budgeting and investing is both practical and empowering. By understanding the difference between needs and wants, allocating funds for savings and investments, and planning for unforeseen expenses, individuals can take control of their finances. This structured approach not only helps in managing day-to-day expenses but also paves the way for long-term financial freedom.

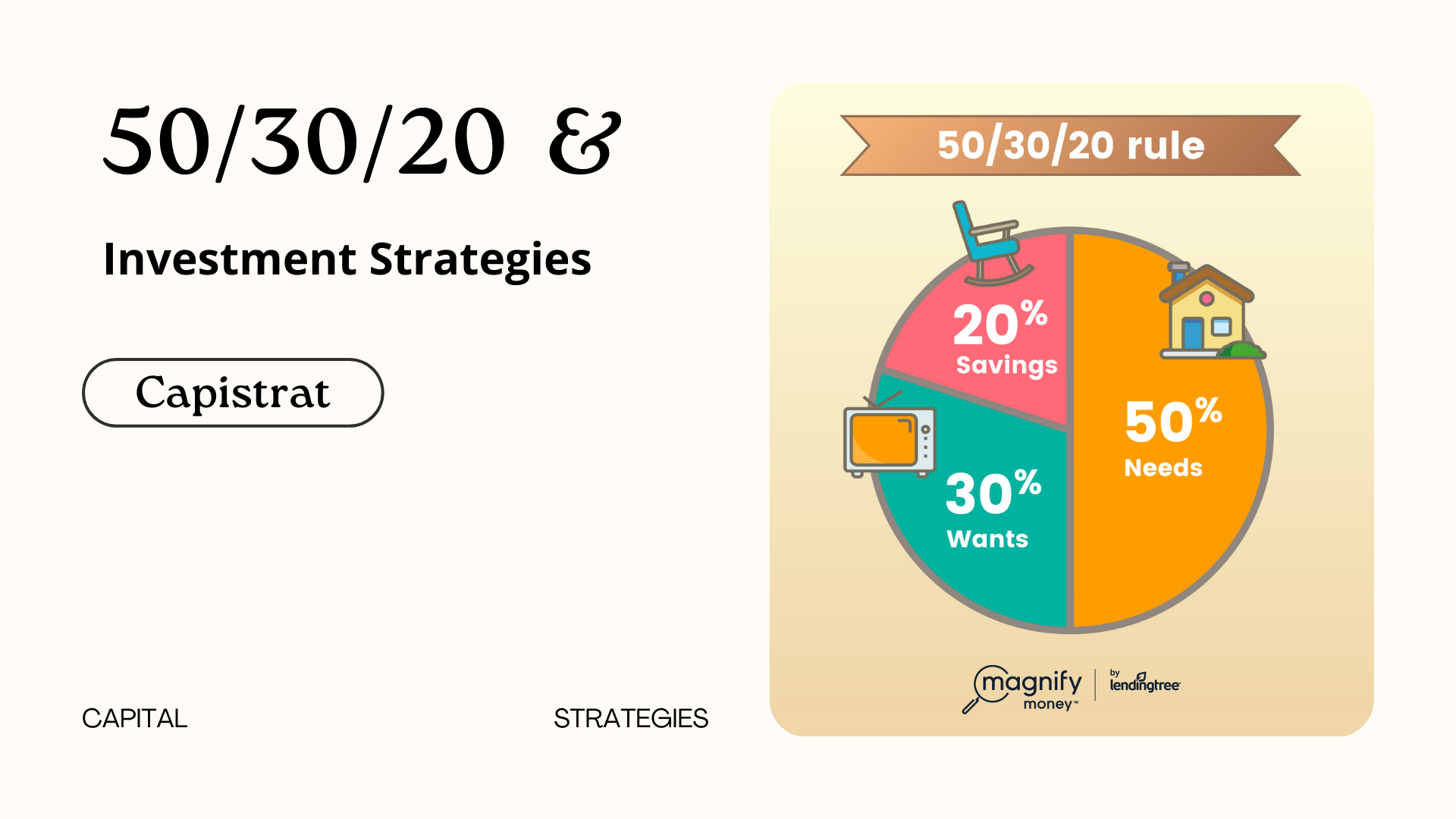

What is the 50/30/20 Budgeting Rule

Suzanne Wanjiko introduces the 50/30/20 budgeting rule, a practical framework for allocating income effectively. Here’s how it works:

- 50% for Mandatory Bills and Expenses

Half of your net income should cover essential needs like rent, utilities, transport, and food. However, Suzanne acknowledges that many people spend more than 50% on these necessities, leaving little room for savings or investments. To achieve financial freedom, it’s crucial to limit mandatory expenses to 50% of your income. - 30% for Savings, Investments, and Debt Repayments

This portion is divided based on your financial priorities. For example, you might allocate 10% to savings, 10% to investments, and 10% to debt repayment. If you’re debt-free, the entire 30% can go toward savings and investments. - 20% for Wants and Miscellaneous Spending

The remaining 20% is for discretionary spending, such as travel, dining out, or social events. Suzanne emphasizes that budgeting isn’t about restriction but about creating guilt-free spending opportunities. This allocation ensures you can enjoy life while staying on track with your financial goals.

The Difference Between Paying and Affording

Suzanne highlights a critical distinction: just because you can pay for something doesn’t mean you can afford it. True affordability means being able to cover a purchase without compromising your savings, investments, or debt obligations. She quotes Jay-Z’s famous advice: “If you can’t pay for something twice, you can’t afford it.” This mindset helps avoid unnecessary debt and ensures financial stability.

Investing: Start with Your Financial Goals

Before diving into investments, Suzanne advises clarifying your financial goals. Whether it’s building an emergency fund, retiring early, owning a home, or generating passive income, your goals will guide your investment decisions. She stresses that investing is personal, what works for one person may not work for another.

Steps to Begin Investing:

- Define Your Financial Goals

List specific, time-bound, and realistic objectives. For example:

- Build an emergency fund (3–6 months of living expenses).

- Achieve home ownership.

- Generate passive income.

- Educate Yourself on Investment Options

Understand the basics of different investment vehicles, such as stocks, bonds, real estate, or mutual funds. Suzanne recommends starting with low-risk options if you’re a beginner. - Match Goals with Investments

Align your financial goals with suitable investment options. For instance:

- An emergency fund should be kept in a liquid, low-risk account like a savings account.

- Long-term goals, such as retirement, may benefit from higher-yield investments like stocks or real estate.

Building an Emergency Fund

An emergency fund is a cornerstone of financial security. Suzanne explains that it should cover three to six months of living expenses and be easily accessible. This fund acts as a safety net for unexpected events, such as medical emergencies or job loss, preventing you from dipping into long-term investments or accumulating debt.

Suzanne’s approach to budgeting and investing is both practical and empowering. By following the 50/30/20 rule, distinguishing between needs and wants, and aligning investments with financial goals, individuals can take control of their finances. This structured approach not only helps manage day-to-day expenses but also paves the way for long-term financial freedom.

Build an Emergency Fund and Match Investments to Goals

Suzanne Wanjiko emphasizes the importance of building an emergency fund, which serves as a financial safety net for unexpected events like job loss or medical emergencies. This fund should cover three to six months of living expenses and be easily accessible. However, she cautions against letting this money sit idle, as inflation can erode its value over time.

To combat this, Suzanne recommends high-yield savings accounts or money market funds. These options offer quick access to funds while providing a modest return (typically 7–9% annually). This way, your emergency fund grows slightly, preserving its value against inflation.

Align Investments with Financial Goals

Suzanne stresses that investing should always align with your financial goals. Here’s how to approach it:

- Define Your Goals

- Short-term: Building an emergency fund.

- Medium-term: Generating passive income.

- Long-term: Retirement planning or wealth accumulation.

- Match Goals to Investment Options

- Emergency Fund: High-yield savings accounts or money market funds.

- Passive Income: Corporate bonds or treasury bonds, which pay interest quarterly or semi-annually.

- Retirement: Stock market investments in stable companies that pay dividends. Suzanne shares her personal strategy of investing in companies like Safaricom and Stanbic, which provide annual dividend checks.

- Understand Risk Appetite

Suzanne highlights the importance of knowing your risk tolerance. Investments come with varying levels of risk:

- Low Risk: Money market funds or treasury bonds.

- Medium Risk: Corporate bonds or real estate.

- High Risk: Stocks or cryptocurrencies. She advises never investing money you can’t afford to lose. Your investment funds should be separate from essential expenses like rent, school fees, or healthcare.

The Golden Rule: Start Small, Think Big

Suzanne’s mantra for investing is to “think big but start small and start now.” She warns against chasing quick money, as this often leads to losses, especially with pyramid schemes or high-risk ventures. Instead, focus on sustainable, long-term growth.

She also underscores the value of financial education. Understanding how different investments work—such as how interest is calculated or the risk profile of each asset—empowers you to make informed decisions. For example, if you prioritize capital preservation, low-risk investments like money market funds are ideal. If you’re aiming for long-term gains, you might tolerate the short-term volatility of the stock market.

Conclusion

Suzanne’s approach to personal finance is both practical and empowering. By following the 50/30/20 budgeting rule, distinguishing between needs and wants, and aligning investments with financial goals, individuals can take control of their finances. Her emphasis on education and calculated risk-taking ensures that even beginners can navigate the world of investing with confidence.

4 responses to “Budgeting, 50/30/20 Rule And Investment Strategies”

-

Is another rule exist than 50/30/20?

-

Yes, many others

-

Yes, many others. The important is to choose what’s right/good for you.

-

-

Now i know how to manage my finances

Leave a Reply